A new analysis presented to the trustees of the Alaska Permanent Fund this week has determined that a proposed solution to Alaska’s multibillion-dollar budget deficit has a 50-50 chance of failing and taking a portion of the fund with it.

On Tuesday, Brian Lawlor and Phil Dobrin of the Connecticut-based investment firm Bridgewater presented the analysis in Anchorage at the trustees’ regular quarterly meeting. They concluded that given the fund’s current makeup, there is only a 52 percent chance that the fund will be able to sustainably supply funding at levels envisioned by the Alaska Legislature.

“Based on history, it’s about a 50/50 chance,” Dobrin said.

According to the latest available figures from the Alaska Permanent Fund Corporation, the fund is worth $62.3 billion. Most of that money — $48.5 billion — is in the fund’s principal, a portion that can’t be spent without a constitutional amendment. The remaining $13.8 billion is in the fund’s earnings reserve. Spending from the earnings reserve requires only a simple majority of the Alaska House and the Alaska Senate, respectively.

Since 1982, the earnings reserve has been used only to pay the annual Permanent Fund Dividend.

That may be about to change in the next few months.

Last year, the Alaska House and Alaska Senate passed different versions of Senate Bill 26, which calls for taking a portion of the earnings reserve each year and using it to pay for state services. The House and Senate are still negotiating their differences, but at their core, the two versions are similar. Each year, fund managers would calculate its average value over the previous five years. Five percent (give or take) of that amount would be taken from the earnings reserve and used for state services, anything from healthcare to pothole patching.

Even under the most optimistic outcome, that money wouldn’t be enough to erase Alaska’s $2.7 billion budget deficit. It would, however, cover as much as three-quarters of that deficit, much more than any tax proposal or budget cut under consideration by the Legislature. Sen. Anna MacKinnon, R-Eagle River, and Rep. Neal Foster, D-Nome, are the chairs of the committee charged with compromising the different House and Senate versions, and they both have told the Empire that they see some version of Senate Bill 26 as the most critical piece of any deficit solution.

“We don’t have an opinion ultimately on which way you should go,” Lawlor told the trustees, but his presentation clearly outlined the drawbacks of the SB 26 idea and how it conflicts with the Permanent Fund Corporation’s mandate.

That mandate, established in a 1976 constitutional amendment, is to “manage the assets of the Alaska Permanent Fund on behalf of current and future generations of Alaskans.”

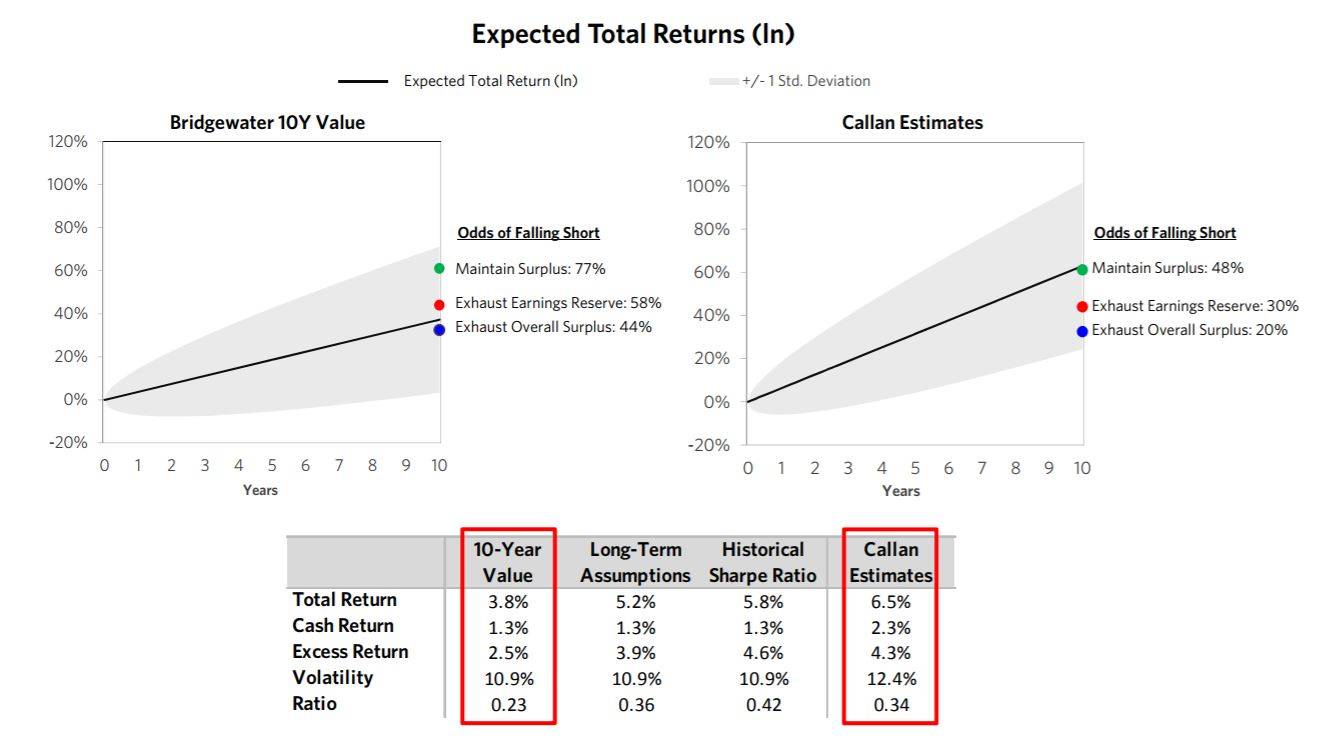

In order to meet the needs of that 5 percent draw from the earnings reserve, and to protect the Permanent Fund’s principal from inflation, the fund would have to earn 6.3 percent annually from its investments. While the fund is currently earning much more than that, both Bridgewater and Callan Associates (the Permanent Fund’s usual outside consultant) don’t expect that situation to last forever.

Callan’s estimates indicate that as it is invested today, there is a 48 percent chance of the fund falling short over the next 10 years. Bridgewater’s estimate for the next 10 years is more pessimistic: It predicts a 77 percent chance the fund will fall short.

Falling short would have severe consequences.

Under normal circumstances, the fund’s earnings reserve acts like a shock absorber. If stock markets decline, money flows from the reserve to the principal, preserving it — under that constitutional mandate — for future Alaskans. Adding a regular 5 percent draw to the earnings reserve would compress that shock absorber like an overloaded pickup truck bed. It would have less flexibility to react to a sudden bump and increase the odds that something would break.

And in Bridgewater’s stress testing, something does break.

Bridgewater has more than a century of data on how various investments react when the economy acts differently. It’s not just how the stock market goes up and down, but how bond markets fluctuate, how real estate prices move, and how even cash itself is worth more or less at a given time. The Alaska Permanent Fund isn’t just invested in stocks; it’s invested in a wide variety of things, all of which react differently under different economic conditions, which means forecasting its performance isn’t straightforward and requires that critical data.

In a series of spaghetti-like charts, Lawlor and Dobrin showed what will happen if the next 10 years of the world economy are like the past 10 years. They showed what will happen if the next 10 years are like the stagflation of the ’60s and ’70s. They predicted what would happen if the next 10 years resemble the Great Depression. There were several scenarios, all taken from the past century and adjusted for the Permanent Fund’s unique mix of investments.

In several cases, the earnings reserve went bust. The principal of the fund stayed safe, but there was no money for government services and little (if any) money for inflation proofing. The fund eventually rebounded, and money again became available for services and inflation-proofing, but sometimes not for multiple years.

The results appeared to sober the trustees.

“You guys are quiet today,” Permanent Fund Corporation director Angela Rodell said at one point in the presentation.

We’re “all in shock here,” one trustee replied.

Lawlor told the trustees that if a 50 percent chance of failure is to high, a lower draw makes sense.

“In our view, 4.5’s a better number,” he said.

After the meeting, Rodell told the Empire that the “probability of failure was much higher than we expected to see intuitively.”

With that in mind, she’s encouraging a lower draw. As director of the Permanent Fund, it’s her mission to follow the constitutional mandate that rests at the heart of the Permanent Fund.

“The less you take, the more likely you’re going to make the goals of continuing to grow the fund and inflation-proof the fund for future generations of Alaskans,” she said.

That’s a policy decision, however, which means the final choice will rest with the Alaska Legislature.

Given the size of the state deficit and the dwindling condition of Alaska’s Constitutional Budget Reserve, that choice will likely be made this year.

The legislative session starts Jan. 16.

• Contact reporter James Brooks at james.k.brooks@juneauempire.com or call 523-2258.

These charts, produced by Bridgewater for the Alaska Permanent Fund Corporation, show that the fund is unlikely to see a return on investments envisioned by Senate Bill 26.